Out of Bounds: Style Drift in the Russell 2000 Value Index

Submitted by Desmond Wealth Management, Inc. on July 3rd, 2021

AMC and GameStop are priced squarely in the large cap growth space and yet represented nearly 1.5% of the Russell 2000 Value Index as of May 31. On the scale of size discrepancies, this is akin to 7-foot-6-inch former NBA star Yao Ming visiting a kindergarten class. However, investors in strategies tracking the Russell 2000 Value Index may be surprised to learn the list of holdings inconsistent with the index’s definition goes much deeper, an outcome of the style drift potentially occurring with most index-based approaches due to infrequent rebalancing.

DRIFTING AWAY

Russell indices undergo an annual reconstitution event at the end of every June during which additions and deletions are made to the list of constituents in accordance with the indices’ rules. For example, the Russell 2000 Value Index constituent list is amended to generally include only value companies below the 1,000th-largest stock in the Russell 3000 Index.

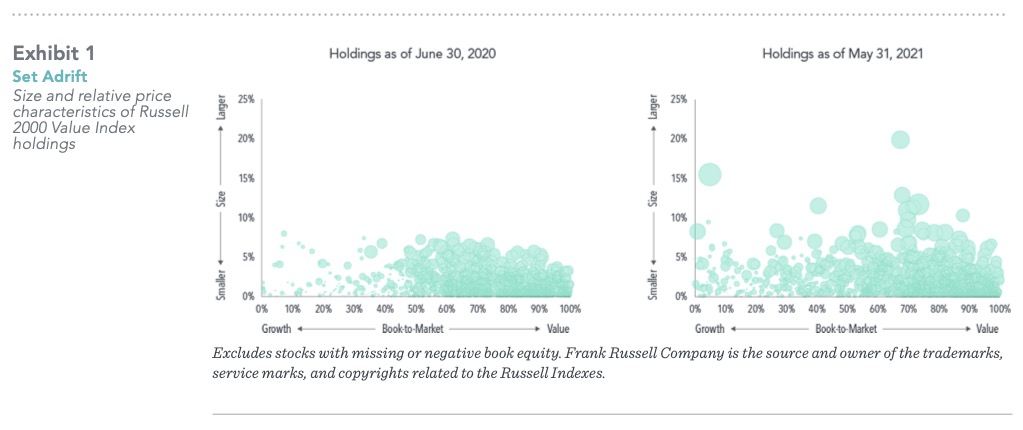

What happens in between these reconstitution events? Imagine skipping lawn mowing duty for a few months and you’ll get the picture. Exhibit 1 illustrates the Russell 2000 Value Index’s holdings at the end of June 2020, following the 2020 reconstitution, compared to its holdings 11 months later, in May 2021. Each bubble represents one stock, plotted based on its percentile rank within the broader Russell 3000 Index on market capitalization (y-axis) and book-to-market ratio (x-axis). The size of the bubble indicates its weight within the index.

The left panel of the exhibit shows an emphasis on the small cap value corner following reconstitution. However, by the end of the following May, many of the index’s holdings have drifted both upward in market cap and toward the growth end of the spectrum. As of May 31, nearly 16% of the index’s weight is accounted for by stocks among the largest 1,000, the domain of Russell’s large cap indices. While GameStop is not the only growth name in the index, its tiny book-to-market ratio of 0.03 combined with its $16.5 billion market cap give it a Yao Ming-like presence in the northwest corner of the style chart.

MISSING THE BOAT?

Research tells us the relative performance of small cap value tends to be delivered by a small subset of the asset class1 and can show up in bunches.2 Both insights are relevant for style drift: infrequent rebalancing can reduce the likelihood of holding the stocks that deliver the premium as well as blunt one’s exposure to the asset class at inopportune times, potentially reducing an investor’s participation in strong runs for small cap value stocks.

Daily portfolio management can potentially spare investors from style drift. Of course, daily rebalancing would likely be prohibitively expensive for a strategy rigidly tracking an index. A flexible daily process that seeks to balance a focus on premiums against short-term drivers of returns, costs and other tradeoffs allows rebalancing of portfolios incrementally through time, keeping them focused on the targeted asset allocation and putting investors in a better position to capture what the market has to offer.

Think of it this way: which oral hygiene approach seems more effective — brushing your teeth for two minutes twice daily or for 24 hours once a year?

1. Eugene F. Fama and Kenneth R. French, “Migration,” Financial Analysts Journal 63, no. 3 (June 2007): 48–58.

2. “An Exceptional Value Premium,” Insights (blog), Dimensional Fund Advisors, October 5, 2020.

This information is intended for educational purposes.

The securities identified do not represent all securities purchased or sold for client accounts. It should not be assumed that an investment in the securities identified was or would be profitable. These materials are not, and should not be construed as, a recommendation to purchase or sell the security identified or any other securities.

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Desmond Wealth Management accepts no responsibility for loss arising from the use of the information contained herein.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.